Federal vs. Private Student Loans: What’s the Difference?

One of the biggest decisions when it comes to student loans is whether to go federal or private. Learn the benefits and tradeoffs of each so you can choose the right fit for your repayment journey.

Key Takeaways

- It’s important to know the differences between federal and private student loans BEFORE you choose one. The loan terms you receive and how repayment is structured impacts the amount you’ll pay in the long run.

- Federal loans offer more repayment options but limit the amount you can borrow. They're generally new borrower-friendly with no credit check (in most cases), fixed interest rates, income-driven repayment plans, and potential forgiveness.

- Private loans can offer more favorable loan terms but depend heavily on your credit score. Private lenders let you borrow more (up to the entire cost of your degree) and may offer better repayment terms, but typically require good credit or a cosigner.

- The right choice depends on your financial situation and goals. No matter which lender you choose, get community support and employer assistance with Paidly.

You’ve heard about federal student loans and private student loans, but what’s the difference? We cover everything you need to know about the pros and cons of each so you can choose the one that’s right for you.

Key Differences of Federal and Private Student Loans

Though federal and private student loans generally work the same way, there are several key differences that’ll affect your repayment.

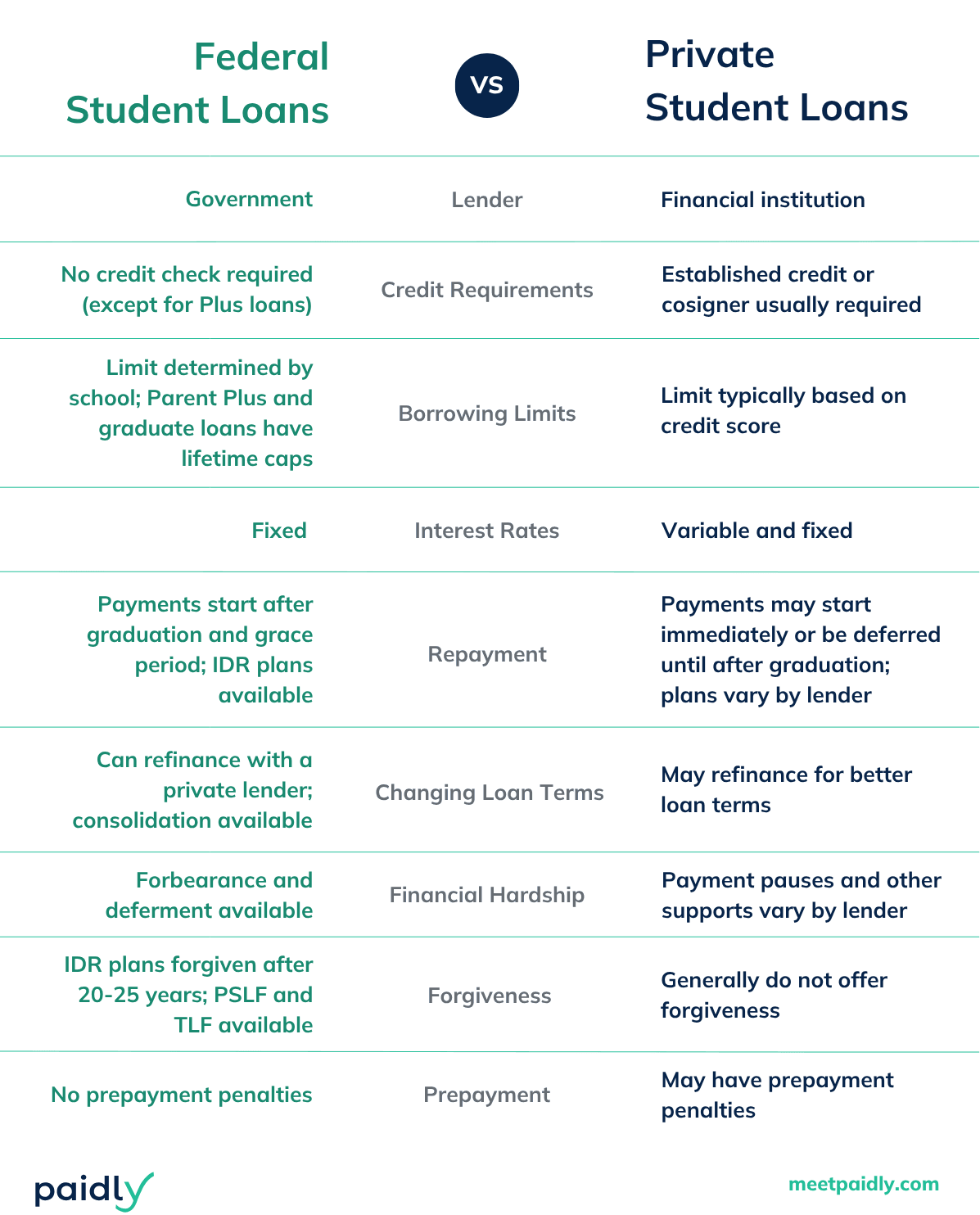

Lender

One of the main differences between federal and private student loans is where the money comes from. Federal loans are funded by the government, and you’ll need to fill out FAFSA to apply for them. Private loans are funded by their financial institution, usually a bank or credit union. To apply for one, you’ll need to go directly to the lender.

Credit Requirements

Another defining feature is whether a credit check is required. Private loans require borrowers to already have established credit, or a cosigner willing to sign with them. Federal loans don’t require either of those things (with the exception of Plus loans).

Borrowing Limits

The type of loan for you may hinge upon how much you need to borrow.

All federal loans take into consideration your financial need, and your school is the one to determine how much you can borrow. Certain federal loans like Parent Plus and graduate loans also have borrowing caps – $65k per student for Parent Plus and a $100k lifetime cap for graduate loans.

Private loans do not have these limits. The amount you can borrow depends on your credit score.

Interest Rates

Your interest rate determines how much you’ll ultimately pay for the loan over time. Having a lower interest rate is a good thing. Federal loans have fixed interest rates, which means your payments and how much you’ll pay over time is predictable. Private loans tend to offer both fixed and variable interest options.

You'll also want to consider when interest starts accruing. In subsidized federal loans, the interest that accrues while you’re still in school is paid for by the government. Unsubsidized federal loans and private loans accrue interest immediately, and you’ll be the one responsible for paying it off.

Repayment Options

Your monthly payment is determined by the amount you borrow, the interest rate, and your repayment timeline. These factors make your monthly payments to private loans pretty straight forward. However with federal loans, you get a few more options based on your circumstances. Income-driven repayment (IDR) plans for federal loans are based on (you guessed it) your income. That means you may pay less each month in order to make those payments more affordable.

Another thing to consider about repayment is when it starts. Federal loans generally do not have to be paid back until after you graduate or stop attending and have a grace period (typically 9 months) until your first payment is due. Private loans either start repayment immediately upon opening the loan or right after graduation.

Changing Loan Terms

Once you’ve had your loan for a while, you may find you want to update loan terms like your interest rate or repayment timeline. Private loans allow you to refinance, or start a new loan from your remaining balance. Refinancing can help you get more favorable loan terms that better match your current situation.

Federal loans can be refinanced to private loans, but not to another federal loan. If you want to combine multiple federal loans, you can consolidate them, which adjusts your interest rate to a weighted average of all your loans.

Financial Hardship

During times of financial hardship, you may be unable to make your monthly payments and need to seek leniency from your lender.

In general, federal loans provide more support and protections. With a federal loan, you have the option to apply for forbearance or deferment, both of which pause your mandatory payments. Some private lenders also provide support during times of economic hardship, but the process and options depend on the lender.

Loan Forgiveness

Another thing to consider is whether you’re eligible for loan forgiveness, or the ability to cancel your remaining balance.

Only federal loans offer forgiveness. If you work in public service, you have the option of working toward Public Service Loan Forgiveness (PSLF) which forgives loans after 120 payments, or Teacher Loan Forgiveness (TLF) which forgives loans after five consecutive years of teaching. Loans on IDR plans also receive forgiveness after 20-25 years (30 years for the new Repayment Assistance Plan).

Private loans generally do not offer forgiveness options.

Prepayment Penalties

Paying your loan off before the scheduled date is a huge feat that will save you money. Federal loans do not have prepayment penalties, or fees for paying your loan off early. Some private loans do, so it’s important to know the loan terms before you start borrowing.

Which Loan is Right for You?

Whether federal or private student loans are a better option for you will all depend on your circumstances. Here are some questions you may want to ask yourself as you consider the type of lender you want:

- Do I have established credit already? If not, do I have someone willing to cosign with me?

- Do the borrowing limits meet my needs?

- Do I need to defer repayment until after I graduate or can I start making payments right away?

- Do I need income-dependent repayment options?

- Do I plan to go into a public service-related field like teaching or medical care?

Assessing the pros and cons of federal and private loans for your specific situation will help you make a decision you feel good about.

Get Support No Matter What You Choose

Regardless of whether you choose a federal or private lender, Paidly helps you get repayment support.

Did you know your employer can help repay your loan? With a Paidly benefit, your employer can directly contribute to your loan on a monthly, quarterly, or annual basis. Plus, with a Section 127 plan, those contributions can be tax-free for them and for you!

No employer benefit yet? You can still crowdfund supplemental payments straight to your loan with the Paidly app, which puts monetary gifts from your community right where you need it most.

All yours in just a few taps

Gain financial awareness and take control of your debt, savings, and donations. Paidly is a convenient, connected way to get ahead with no pay-to-download or hidden fees.

Learn more about getting employer support and crowdfunding student loans with Paidly.

Student Loans Don’t Have to Be Daunting

Whether you’re just starting out or going back to school, choosing the right loan for you is a big decision. Reviewing the benefits and drawbacks of each will help you make a confident choice. Consider your credit, borrowing needs, career plans, and whether you’ll need flexible repayment or forgiveness options.

Know that the loan you start with doesn’t have to be the loan terms you keep forever. Changing your federal repayment plan or refinancing to a private lender are ways to adjust your loan to fit your circumstances. Plus, no matter which loan you pick, you can get community support and employer assistance to help you along the way.

Want to know more about borrowing? See our ultimate guide to taking on student loans.

Samantha Park

Samantha Park is a writer with a background in public service work. She earned a M.S. in Professional Writing from Towson University where she focused on writing for the private and public sectors, and has previously graduated with an A.A. in Psychology from Anne Arundel Community College and a B.A. in Sociology from the University of Maryland College Park. Samantha has worked within and alongside the public sector for over a decade and cares deeply about empowering marginalized youth, expanding access to opportunity through education, and increasing community involvement.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.

How the Big Beautiful Bill Affects Student Savings

OBBBA expanded 529 plan uses, made ABLE provisions permanent, and introduced Trump Accounts. Here’s what you need to know.