Navigating Public Service Loan Forgiveness

You might have heard that some student loans are eligible for public service loan forgiveness or PSLF, but what does that mean? What jobs qualify, and how do you apply?

, Teacher looking at a complex chalkboard , Paidly")

Key Takeaways

- Public Service Loan Forgiveness (PSLF) is designed to relieve government and non-profit workers of federal student loan debt

- Eligible borrowers must work full-time and have a Federal Direct Loan on an Income-Driven Repayment plan or 10-year Standard Repayment plan

- 120 qualifying monthly payments must be made before the remaining balance is forgiven

- The future of PSLF is uncertain - it’s important to consider other avenues like Employer Student Loan Repayment assistance to help pay down debt

Public Service Loan Forgiveness (PSLF) was created to relieve full-time public service workers of federal student loan debt. PSLF is structured to forgive the remaining balance on Federal Direct Loans after making 120 qualifying monthly payments under a qualifying repayment plan. While PSLF aims to provide relief to student loan borrowers, the future of the program is uncertain. Read on to learn about PSLF eligibility, how to apply, and other avenues to pay off debt while working in public service.

What is Public Service Loan Forgiveness (PSLF)?

Public Service Loan Forgiveness (PSLF) is a federal program that forgives the remaining balance of your federal student loans after you make 120 monthly payments on an Income-Driven Repayment plan (IDR) or a 10-year Standard Repayment plan. The program is designed to help borrowers who have made regular payments on their student loans for at least 10 years. The goal of PSLF is to allow people who are working in public service jobs - like teachers, medical staff, and police officers - to get out from under their debt burden.

Glossary: PSLF and IDR

- PSLF (Public Service Loan Forgiveness): A program that forgives the remaining balance of eligible Federal Direct Loans after meeting specific requirements, including making 120 qualifying payments while working for a qualifying employer.

- IDR (Income-Driven Repayment): An umbrella term for four repayment plans that base your monthly payment on your income and family size, potentially lowering your monthly payments and increasing the timeline for repayment.

Who Qualifies for PSLF?

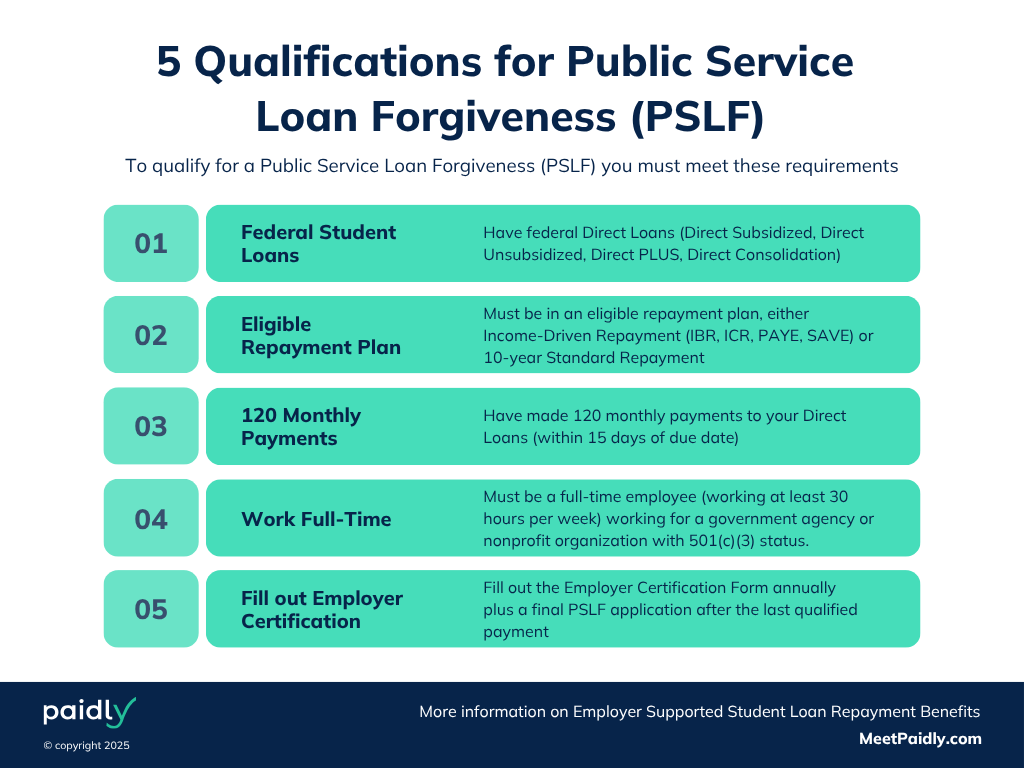

PSLF is only available to full-time employees of qualifying employers that meet certain requirements. To qualify for PSLF, you must:

- Have an eligible federal student loan (specifically, Federal Direct Loans)

- Work for a qualifying employer (government organizations, non-profit organizations, or other qualifying public service jobs)

- Be a full-time employee (working at least 30 hours per week)

- Make 120 monthly payments on your Direct Loans under an Income-Driven Repayment plan (IDR) or a 10-year Standard Repayment plan

- Complete the required Employer Certification Forms (ECF)

What Jobs Qualify for PSLF?

Jobs that typically qualify for PSLF include:

- Employment in government. If you work for a government agency or non-profit entity, then the PSLF program is an option for you. This includes teachers (including those who teach at charter schools), law enforcement officers, military personnel, public defenders and prosecutors, healthcare workers, and other occupations that are considered public service.

- Employment in nonprofits with 501(c)(3) tax-exempt status. If you work for a non-governmental nonprofit organization, PSLF is an option for you. This includes most nonprofit and charitable organizations.

- Employment in nonprofits without 501(c)(3) status. If you work for a nonprofit that provides specific public services, such as education, health, or public safety, then PSLF may be an option for you.

What Loans Qualify for PSLF?

To participate in PSLF, your loans must be in the Federal Direct Loan program. Eligible loan types include:

- Direct Subsidized Loans. These are loans for undergraduate students with demonstrated financial need, and the interest is paid by the federal government while you are in school and during certain deferment periods.

- Direct Unsubsidized Loans. These loans are available to both undergraduate and graduate students, and the interest accrues while you are in school and during deferment or forbearance.

- Direct PLUS Loans. These loans are available to graduate or professional degree students, as well as parents of dependent undergraduate students. The borrower is responsible for paying all the interest that accrues, and they require a credit check.

- Direct Consolidation Loans. These loans allow you to combine multiple federal student loans into a single loan, simplifying your repayment process.

It’s important to note that Federal Family Education Loans (FFEL), Federal Perkins Loans, and private loans are not eligible for PSLF - only Federal Direct Loans qualify. However, consolidating non-eligible loans into a Direct Consolidation Loan can make them eligible.

How do I know if I have FFEL Loans?

If you have federal student loans issued in 2010 or prior, chances are high that they fall under the Federal Family Education Loan Program (FFEL). A portion of these outstanding FFEL loans remain under the control of the federal government, known as ED-held FFEL loans, while the majority continue to be managed privately by corporations, such as Nelnet.

You can visit studentaid.gov to determine the type of student loan you're dealing with and see if it's under the jurisdiction of the federal government or owned by a private entity. Use your FSA ID to see your loan amount, status, servicer, and any outstanding balance.

Do I Need to Be on an Income-Driven Repayment Plan?

While it's not an absolute requirement to be on an Income-Driven Repayment (IDR) plan to qualify for Public Service Loan Forgiveness (PSLF), we highly recommend an IDR plan if you’ll be using PSLF. These plans take into account your income and family size, providing more budget-friendly monthly payments. Moreover, an IDR plan ensures that your monthly payment contributes towards the required 120 payments for the PSLF program.

Although payments on the 10-year Standard Repayment plan qualify, it’s beneficial to switch to an IDR plan to maximize the PSLF advantages. Ordinarily, the 10-year Standard Repayment plan results in fully repaying your loans once you've made 120 qualifying PSLF payments, leaving no remaining balance to forgive unless you’ve had approved periods of deferment or forbearance.

How Do You Apply for PSLF?

To apply for PSLF, you need to submit the Employment Certification Form (ECF) to your student loan servicer. This form asks you to provide proof that you're working in a qualifying public service job and provides information about the employer you work for. Applying for PSLF involves these essential steps:

- Review your loan portfolio to ensure you have eligible Federal Direct Loans

- Ensure your employment qualifies for PSLF by completing and submitting the Employment Certification Form annually and with each change of employer

- Choose a qualifying repayment plan (IDR plans are recommended)

- Make the required 120 qualifying monthly payments

- Submit the PSLF application after completing the 120 payments

What is Temporary Expanded PSLF (TEPSLF)?

Temporary Expanded Public Service Loan Forgiveness (TEPSLF) is a temporary expansion of the PSLF program that allows borrowers who were previously ineligible for PSLF due to being in a non-qualifying repayment plan (such as graduated or extended) to receive forgiveness if they meet other PSLF requirements, including making 120 qualifying payments.

What is Teacher Loan Forgiveness (TLF)?

For qualifying teachers who don’t have large amounts of debt, Teacher Loan Forgiveness (TLF) forgives less debt but offers it quicker.

Who Qualifies for TLF?

Teachers who have taught full-time for five consecutive years at a qualifying low-income elementary or secondary school qualify. To qualify for TLF, you must:

- Have worked full-time as a qualified teacher for five consecutive years (at least one of those years must have been after the 1997-1998 academic year)

- Have an eligible federal loan (Federal Direct Subsidized, Federal Direct Unsubsidized, or Subsidized Federal Stafford, or Unsubsidized Federal Stafford)

TEPSLF will only be available until a certain amount of loan forgiveness has been granted, so it’s imperative you apply as soon as possible.

How Much is Forgiven with TLF?

Special education teachers and secondary math and science teachers can get up to $17,500 forgiven. Elementary school teachers and secondary school teachers who teach other subjects can get up to $5,000 forgiven.

How Do You Apply for TLF?

- Verify that you meet the eligibility requirements

- Submit a completed Teacher Loan Forgiveness Application to your loan servicer

Ease Repayment with Paidly

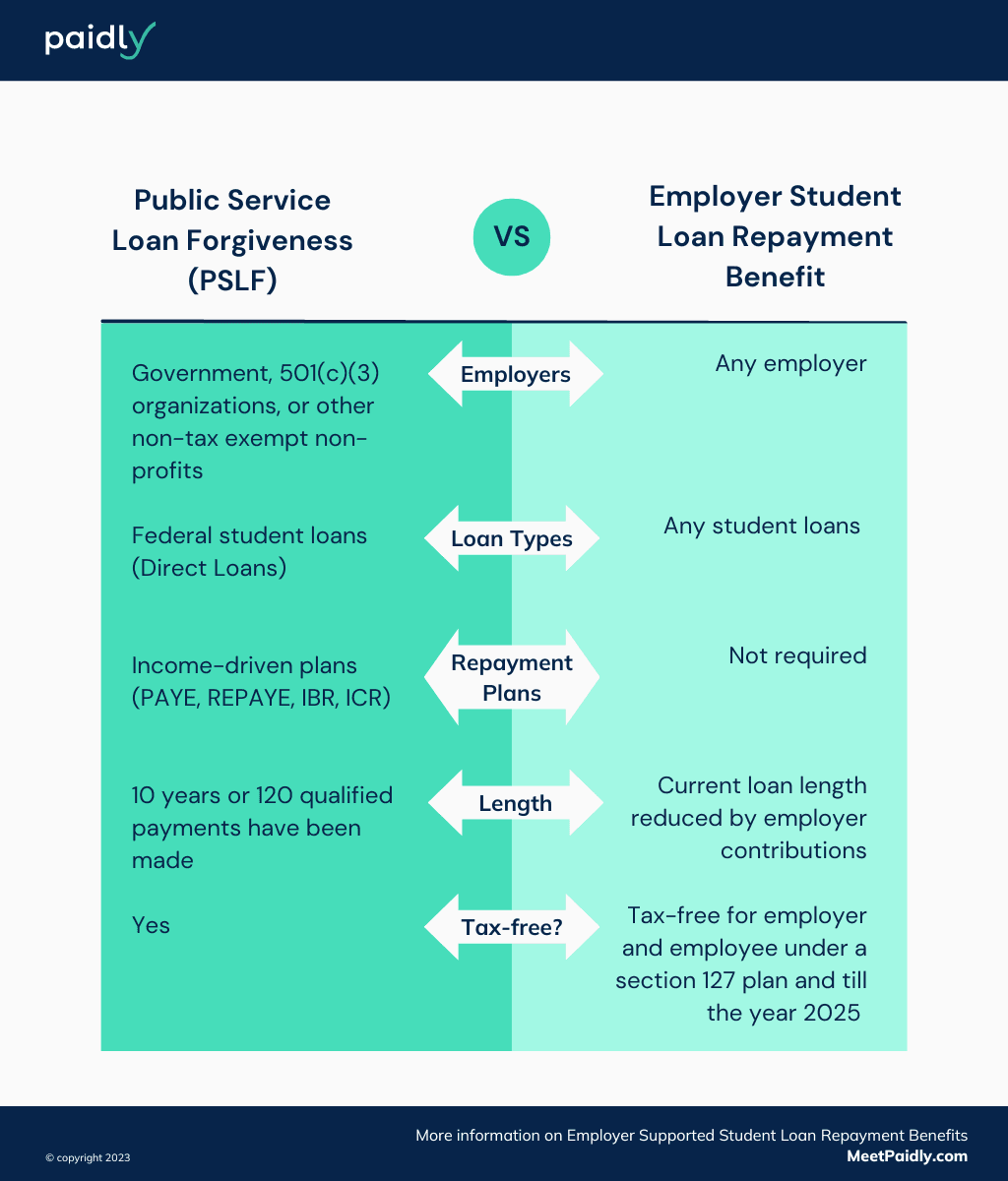

Given the uncertain future of PSLF and federal loan forgiveness, it's crucial to consider additional avenues for alleviating the stress of student loan debt. Paidly offers innovative solutions that bridge the gap between financial freedom and student loan obligations.

Ask for Employer Assistance

Forward-thinking employers can offer Employer Student Loan Repayment to help pay off employee loans by integrating Paidly into their benefits programs.

Paidly not only empowers public service workers to regain control of their student loans but also significantly eases the financial burden affecting their everyday lives. Employers can make a difference and embrace this opportunity to drive positive change by providing tax-free supplemental payments of up to $5,250 annually to employees.

Talk to your employer or HR department to see if an Employer Student Loan Repayment benefit is available to you. If they don’t offer assistance yet, make a case for the benefit using our step-by-step guide.

Employer Support Not An Option?

If your employer cannot provide repayment assistance, it may be time to seek support from your community. Check out Paidly’s app, which provides a safe and easy way for family and friends to help pay down student loans.

For more information, see our Insider's Guide to PSLF.

Team Paidly

Paidly is the go-to platform for rising above student debt. We specialize in innovative solutions, such as employer student loan assistance benefits, streamlined 529 plan contributions, and crowdfunding tools for individuals and their families. Backed by nearly two decades of experience in financial technology, Paidly is committed to simplifying student loan repayment, reducing loan dependency, and empowering students to take control of their finances no matter where they are in their educational journey.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

Education Benefits You Should Know About

Education benefits like 529 savings, tuition reimbursement, and student loan repayment can help you reduce education costs during every stage of your career.

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.