Solving the PT/OT Shortage with Student Loan Benefits

High student debt and low starting pay are burning out physical and occupational therapists. With an impending shortage, employer student loan assistance could turn the tide.

Key Takeaways

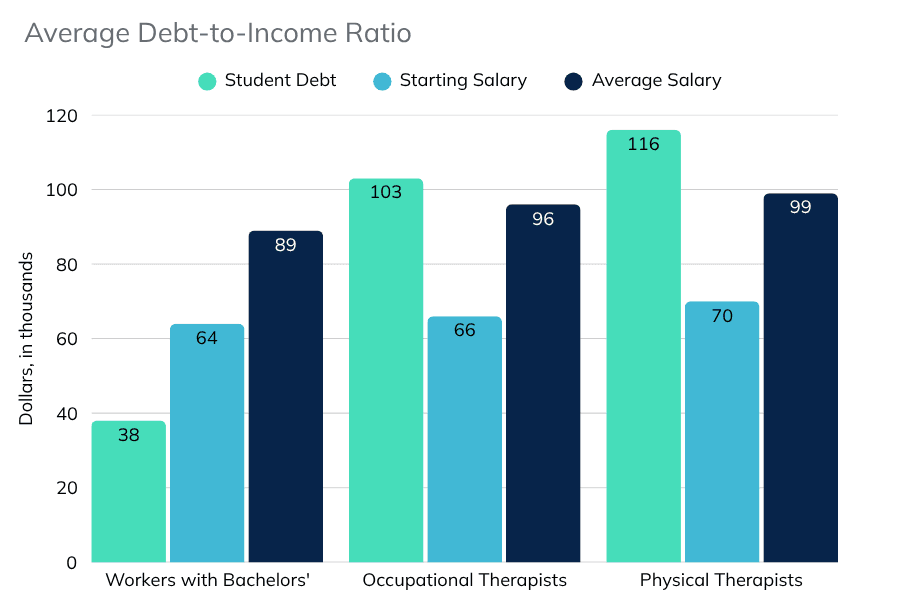

- Physical Therapists (PTs) and Occupational Therapists (OTs) carry significant student debt. The average rehabilitative therapist owes $103k in loans and has a debt-to-income ratio of 197%.

- High student debt and low starting salaries cause anxiety and burnout. 84% with physical therapy debt feel their salary is not enough to manage their student loan payments.

- Employer student loan assistance could eliminate the rehabilitative shortage. 80% of PTs and OTs have student debt, but only 8% are receiving student loan assistance.

- Paidly helps healthcare employers offer student loan repayment benefits to their employees. Talk to an Expert to see how Paidly works with your staff.

Physical Therapists (PTs) and Occupational Therapists (OTs) play a crucial role in helping individuals regain independence and mobility after injury, illness, or disability. And with an aging population, rehabilitative careers are becoming more important every year.

However, the rising cost of education and the resulting student debt crisis pose a significant threat to the healthcare industry. PTs and OTs in particular take on more student debt than their starting salaries can handle, leading to long-term financial struggle that results in anxiety, burnout, and in some cases, resignation.

In this article, we explore the factors contributing to the impending rehabilitative care shortage, the burden of average student loan debt for physical and occupational therapy graduates, and how employer benefits offer a critical solution.

Rehabilitative therapists are drowning under student loan debt

Student loan debt is a direct contributor to low job satisfaction in the healthcare industry. This is especially true of physical and occupational therapists, whose debt-to-income ratio makes it difficult for them to pay back the cost of entering their profession.

Rising Cost of School and Licensure

Entry to a career as a rehabilitative therapist requires a graduate degree from an accredited program: Doctorate of Physical Therapy (DPT) for PTs and Master’s in Occupational Therapy for OTs. These programs cost years of education and tens of thousands of dollars - and the price is climbing. In the last five years alone, physical therapy doctoral program tuition has jumped 12%.

This upward trend is not just impacting rehabilitative therapists. According to the Center on Education and the Workforce, college costs have increased 169% over the last four decades, while earnings for workers between 22 and 27 have only increased by 19%. Escalating tuition fees mean many graduates begin their careers burdened with substantial debt.

For PTs and OTs, the burden of entry doesn’t end with a degree. Beyond tuition, certification and licensure come with their own price tags. Rehabilitative therapists require a license to practice, which means passing an exam and paying for registration and occasional renewal - and these costs add up quickly.

Minimum Cost of Entry

| Physical Therapy | Occupational Therapy | |

|---|---|---|

| Average Tuition | $116k | $89k |

| Exam Cost | $485 + $112 testing center fee | $540-$595 (online or in-person) |

| Initial Licensure | $13-$450 (varies by state) | $25-$400 (varies by state) |

| Total | $116,610-$117,047 | $89,565-$89,995 |

In New York, a newly licensed PT can expect to spend over $1,500 just on the exam and maintaining licensure in their first ten years. OTs face similar costs, exceeding $1,700 over the same period. These expenses are not always covered by employers, adding significant pressure right from the start of their careers and further pushing back their ability to pay down loans.

The barrier of entry is a financial issue - which means talented individuals may be discouraged from pursuing rehabilitative therapy solely due to the cost.

Debt to Salary Ratio

High debt and low pay early in their careers makes it difficult for new PTs and OTs to pay off the price of education, which means accrued interest and getting even deeper in debt.

The average student debt for rehabilitative therapists is $103k. Many new PTs and OTs have an average total debt-to-income ratio of 197% - meaning they owe almost double their annual earnings. With starting salaries below $70k and median salaries just under $100k, rehabilitative therapists complete more education and take on more than double the debt yet make roughly the same amount as the average bachelor’s degree holder.

The Consumer Financial Protection Bureau says students should not borrow more than their expected starting salary one year after graduation - which means PTs and OTs must enter the field knowing they are taking on a debilitating amount of debt in order to serve the public.

This is especially hard to swallow when PTs have less earning potential than other healthcare professions that require a doctorate. For example, physicians on average make upwards of $240k while the average salary for physical therapists is only $99k.

Exploring Repayment Paths: Loan Forgiveness vs. Reality

Many rehabilitative therapists hope to rely on programs like Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) plans to help manage their massive student debt. While loan forgiveness programs can be valuable for eligible individuals in qualifying public sector jobs, the requirements can be strict, the application process complex, and the long-term availability uncertain.

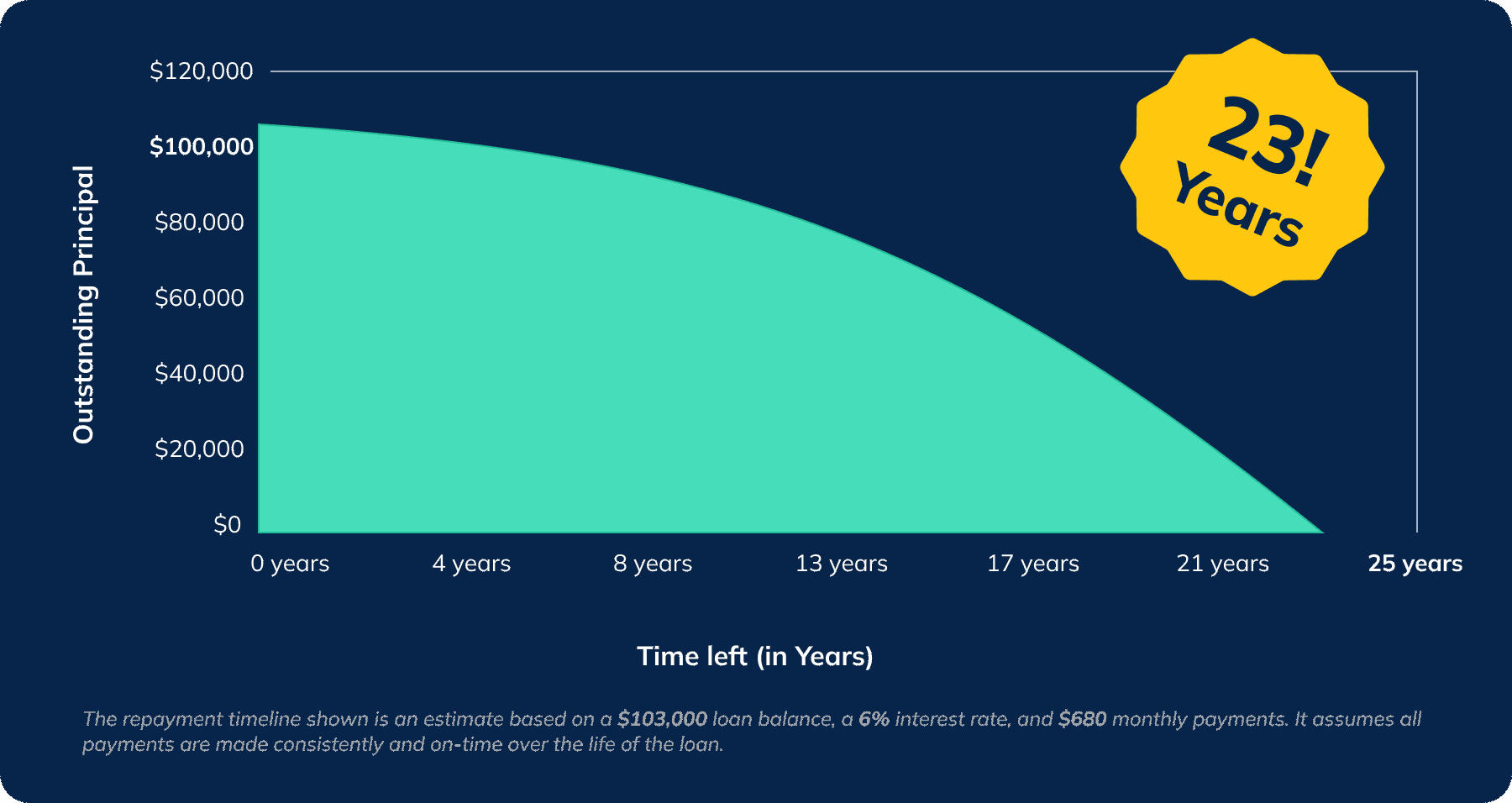

Without reliable loan forgiveness, consistent student loan assistance, or aggressive personal payments, many rehabilitative therapists will take decades to pay off their physical therapy debt, making it a career-long financial burden. Even contributing 10% of their monthly income at a 6% interest rate could mean nearly 25 years of payments and over $90k in interest – enough for an occupational therapist to pay for their entire education over again.

Quality of Life and Career Satisfaction

Debt owed isn't just a number PTs and OTs chip away at - it affects quality of life and career satisfaction.

Student debt has long-term consequences and a vast majority of PTs feel their salary isn’t sufficient to manage their student loans. Because of this, many rehabilitative therapists report significant delays in achieving important personal milestones. For example, 60% delay buying a home, 56% delay contributing to retirement savings, and more than half postpone starting a family because of their debt.

Not only does student debt have a financial toll, it also has an emotional and psychological impact. 70% of physical therapists feel “persistent anxiety” due to their student debt. Consistent stress is a gateway to professional burnout, and student debt is a lead contributor.

One study warned that we should expect negative career satisfaction as the burden of student debt grows heavier:

“Considering the alarming rate with which educational debt is rising among newly graduating physical therapists, one would expect much poorer job satisfaction and retention within the profession in the next 20 years.” (NIH)

The financial constraints caused by excessive debt and the resulting burnout may push some therapists to reconsider their chosen path.

According to one study, some OTs are rethinking their career decision despite overwhelmingly loving their jobs. Many say they would reconsider going into rehabilitative therapy due to the financial struggle they face as a result. Clearly, job satisfaction cannot be bolstered by passion alone.

When nearly half of surveyed therapists feel less optimistic about rehab’s future, it is clear that the student debt crisis is not only a personal financial issue but a broader systemic concern that could affect workforce stability and patient care quality.

We cannot afford to lose rehabilitative therapists, especially when we’re about to need more than ever.

Rehabilitative Care Shortage

Both physical therapy and occupational therapy are experiencing stronger than average job growth. This is mainly due to the aging of the Baby Boomer generation, all of whom will be “Medicare age” by 2030. With an increased need for rehabilitative care as older adults remain active and live longer, more PTs and OTs will be needed.

However, we are headed for a rehabilitative shortage which threatens care quality and access. Student debt is a major driver pushing professionals out of the field and discouraging new entrants. Experts warn that without more PTs and OTs, we’ll have a significant rehabilitative shortage by 2037.

This scenario could ultimately impact patient care, as a burned out workforce struggles to meet the rising demand for rehabilitative services. If we want to have enough PTs and OTs to care for the public, we need to start making changes to improve their career satisfaction.

Employer student loan assistance could avert the rehabilitative care shortage

Better compensation elsewhere was one of the top three reasons PTs and OTs choose to resign. The good news: there’s something employers can do about that!

Rehabilitative therapist wants are clear: lessen financial struggle to keep and attract the workforce. The American Physical Therapy Association (APTA) recommends reducing educational costs, improving wages, and expanding employer-based student loan repayment programs in order to retain skilled therapists.

According to APTA, delaying those who voluntarily leave the field by 2 years would eliminate the impending rehabilitative therapy shortage. One of the key ways employers can retain their staff is by helping to repay loans since employer student loan assistance prolongs employees’ commitment to their companies by 5 years or more.

Offer Student Loan Assistance with Paidly

Student debt burdens 80% of physical and occupational therapists, but only 8% are receiving employer student loan assistance. Offering assistance is an effective way to retain and support rehabilitative staff, and with the uncertain future of loan forgiveness programs PTs and OTs typically qualify for, it’s vital they receive employer support to pay off their loans.

Healthcare organizations can partner with student loan assistance services like Paidly to provide support in managing and reducing the debt of their staff. Contributing even $50 a month toward a rehabilitative therapist’s student debt could save them over $10k in interest and 3 years of repayment.

With Paidly, employers help relieve the debt burden in a way that maintains employee confidentiality and streamlines the payout process. In addition to regular, monthly payments, employers can also pay bonuses and PTO buyback directly toward employee student debt.

Employee student loan assistance services

Easily offer student loan repayment benefits. Download our free guide or visit our employer benefit page to learn how to relieve employee financial stress.

Download

It’s not too late to turn the tide

“While providing optimal care and leading the charge in healthcare delivery remains a top priority for the practice of the future, it cannot be done without a healthy workforce.” (WebPT)

If we want to maintain a strong and motivated rehabilitative workforce, employers must tackle student debt head-on. By lowering the financial burden of education and investing in skilled physical and occupational therapists through student loan assistance, employers can secure a healthier future for the public and for their employees.

Ready to get started?

Samantha Park

Samantha Park is a writer with a background in public service work. She earned a M.S. in Professional Writing from Towson University where she focused on writing for the private and public sectors, and has previously graduated with an A.A. in Psychology from Anne Arundel Community College and a B.A. in Sociology from the University of Maryland College Park. Samantha has worked within and alongside the public sector for over a decade and cares deeply about empowering marginalized youth, expanding access to opportunity through education, and increasing community involvement.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.

How the Big Beautiful Bill Affects Student Savings

OBBBA expanded 529 plan uses, made ABLE provisions permanent, and introduced Trump Accounts. Here’s what you need to know.