How Does Student Loan Interest Work?

If you're a recent graduate, odds are that you have student loans to repay. When you get a student loan, you also have to pay interest on the money you borrow.

Key Takeaways

- Understand the difference between loan interest and principal, and how they affect your monthly payments and the total amount you owe.

- Learn about the two types of interest, simple and compound, and how they're calculated on your student loan principal balance.

- Discover the impact of employer contributions on reducing your student loan debt, and strategies to pay off your loans faster.

When you take out a student loan your payments are broken into two parts: loan principal and loan interest. But did you know that there are two different ways that interest can be calculated? This can make a big difference in your monthly payments and how much money you owe in total.

Understanding How Student Loan Interest Works

What is loan interest?

Interest is the cost of borrowing money. It's calculated based on the amount borrowed, the length of the loan and an interest rate. Interest is added to your loan balance at regular intervals (usually monthly) so that you will pay more over time because it compounds.

The amount of interest you pay depends on how much money you borrow and for what period of time, as well as the interest rate tied to your loan. The higher the interest rate, the more you'll have to pay in total if you keep borrowing money over time.

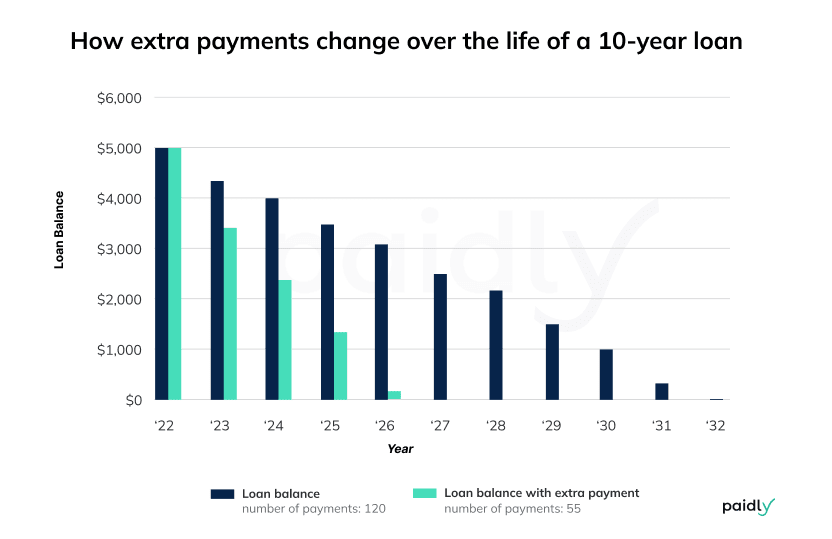

For example, let's say you take out a $5,000 student loan today in 2022 at 6% interest with a 10-year repayment period. That means you'd have to make monthly payments of $56 for 10 years in order to pay off all your debt—you'll end up paying $1,649 in just interest! Your loan won't be paid off until 2032.

With an employer contribution of an extra payment of $50 through Paidly—you'll end up paying $716 in interest. That saves you $923 in interest alone, as well your loan will be paid off in 2027, five years sooner!

The higher the interest rate, the larger the amount of interest you'll pay.

Interest is added to the principal balance and charged on that sum. In other words, if your student loan has a 5% interest rate and you make no payments during one month, then after that month your principal balance will be $500 + ($500 x 0.05) = $525.

What is principal?

Principal is the original amount you borrowed. When you make a payment, it is typically applied to the payment fees first, as late fees, then to interest charges. If any money is left over it then will apply to the principal balance of your loan.

As you pay down your student loan balance, the interest rate is applied to a lower principal amount each month, which results in less of your payment going toward interest charges, fees, and more of your payment going toward your student loan principal balance.

Extra monthly payments in addition to your minimum monthly payment which includes interest will go directly toward the principal balance which will result in paying down your principal faster than your scheduled payment plan, which can save you in both time and money. A great way to see how making an extra payment on your loan reduces the life of your loan, review the image found under what is loan interest above or checkout our student loan payoff calculator.

But be aware, some loan providers may charge you prepayment penalties if you pay your loan off early. Make sure to read the fine print so you do not get charged a fee for paying your loan off early.

Interest vs Principal

The difference between paying interest and paying off your principal is a little bit like the difference between buying something at a store and buying stock in that company. When you pay interest, you’re simply paying for the privilege of using the money. You don't actually "own" anything with this kind of payment—you just get to use it on credit for a while.

When you pay off your principal, however, it's more like purchasing an item outright with cash: you own what you bought. With student loans, paying off your principal means that once all payments have been completed (or as much as possible), there will be no more debt outstanding—just like when you buy an item with cash instead of using a credit or debit card because there's nothing left outstanding after purchase.

There are two kinds of interest, simple and compound

What's the real difference between simple interest and compound interest? It's definitely worth grasping if you're navigating student loans. So, let's break it down:

-

Simple Interest: It's straightforward. This type is calculated just using the principal amount you initially borrowed.

-

Compound Interest: This one's a bit more complex. It's calculated based not only on your original loan, but also on the interest that has already gathered over time.

Understanding these key differences could really empower your decision-making when it comes to managing and paying off your student loans.

How is Principal Paid

When you make monthly payments, the principal will be paid off over time. As your monthly payments are processed, some of the money is applied to interest and some goes toward paying down your principal balance. This means that if you have a $10,000 student loan at 6% interest with five years left in repayment, it will take you 50 months (5 years) and $6,750 ($10,000 x 6%) in interest to repay your loan if all of your monthly payments go toward paying down that amount. As you continue to make payments, you’ll start to pay more in principal and less in interest.

How to Identify your loan principal

As you are paying down your student loans, it is important to know how much of that payment is going toward principal and how much is going toward interest. Your monthly loan statement and other resources like your loan contract or servicer website will help you identify what portion of the payment you make each month reduces the amount owed on your student loans.

You can also call or email customer service for your loan servicer, with questions about what portion of your monthly payment goes to principal versus interest.

Empowering Your Path to Effective Student Loan Repayment

With understanding the difference between interest and principal, it’s time to start paying off those student loans. The best way to do this is by creating a budget and sticking to it! Make sure your monthly payments include both the interest due on your loan as well as some money towards paying off your principal balance each month until it gets paid off completely. Asking your employer to provide educational assistance or a student loan repayment benefit through Paidly's employer benefit will allow you to pay down your loans even faster.

Team Paidly

Paidly is the go-to platform for rising above student debt. We specialize in innovative solutions, such as employer student loan assistance benefits, streamlined 529 plan contributions, and crowdfunding tools for individuals and their families. Backed by nearly two decades of experience in financial technology, Paidly is committed to simplifying student loan repayment, reducing loan dependency, and empowering students to take control of their finances no matter where they are in their educational journey.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.

How the Big Beautiful Bill Affects Student Savings

OBBBA expanded 529 plan uses, made ABLE provisions permanent, and introduced Trump Accounts. Here’s what you need to know.