Child Savings Accounts: Coverdell ESAs vs. 529 Plans vs. Trump Accounts

Trump Accounts offer more flexibility but less tax advantages than 529 plans and Coverdell ESAs. Learn how these child savings options compare so you can pick the best fit for your child’s future.

Key Takeaways

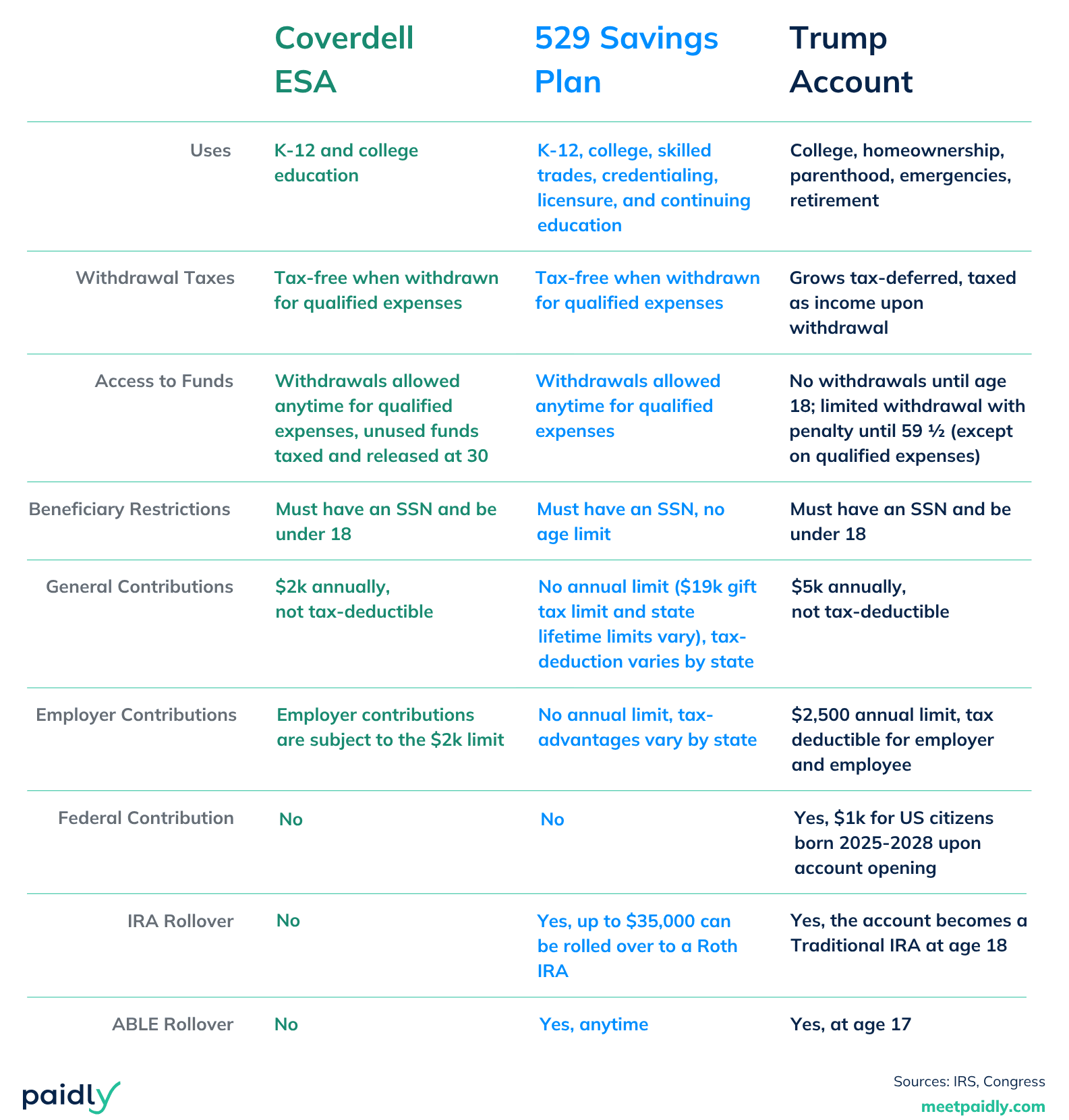

- Trump Accounts can be used on the widest range of expenses, covering college, homeownership, parenthood, emergencies, and retirement. Coverdell ESAs and 529 plans are specifically for K-12 and higher education, with 529s also covering career upskilling.

- 529 plans and Coverdell ESAs offer tax-free withdrawals for qualified education expenses, while all Trump Account withdrawals are taxed.

- 529 plans generally have the highest contribution flexibility, while Coverdells and Trump Accounts have annual contribution limits and age restrictions.

- Families can build savings through personal contributions, community crowdfunding, and employer benefits. Learn more about your support options with Paidly.

Trump Accounts (or 530As) are joining a growing list of child savings options alongside 529 plans and Coverdell ESAs. While all three help families prepare for future education costs, each account works differently when it comes to taxes, contribution limits, flexibility, and long-term use.

Let’s get into the differences between these child savings options and how to choose the right one for your family.

Why Build College Savings?

Starting a savings account for a child or loved one is one of the best ways to give them a financial head start. Even small contributions made early can grow significantly over time.

One of the largest expenses many families face is education. College costs have risen dramatically over the past several decades, far outpacing wage growth. Preparing ahead of time – even if savings only cover part of the cost – helps reduce reliance on student loans and eases future financial stress.

Coverdell ESAs vs. 529 Plans vs. Trump Accounts

Here’s an overview of the three main child savings options:

-

Coverdell Education Savings Accounts (ESA). Coverdell ESAs are custodial-style education savings for children. Funds can be used for qualified K-12 and college expenses, but contributions are capped at $2,000 annually.

-

529 Savings Plans. 529 plans are state-sponsored education savings accounts available for both children and adults. They can be used for a broad range of education-related expenses, including credentialing programs and continuing education.

-

Trump Accounts (530A). 530As are custodial-style Traditional IRAs for children. They offer the most flexibility of the three options and can be used for education, homeownership, childbirth or adoption, emergencies, and retirement.

What’s the Difference?

The biggest differences between these accounts come down to what the funds can be used for, how withdrawals are taxed, whether there are contribution limits, and what happens to unused funds.

Covered Expenses

All three account types can be used for education expenses (Coverdell and 529 cover K-12 in addition to higher education). 529s and Trump Accounts can be used for other expenses, as well.

529 plans cover lifelong education:

- Skilled trade programs

- Credentialing and licensure fees

- Continuing education

Trump Accounts offer even broader flexibility:

- First-time homeownership (up to $10,000)

- Birth or adoption expenses (up to $5,000)

- Emergency expenses (up to $1,000 annually)

Tax Advantages

All three account types grow tax-deferred, but they differ significantly in how withdrawals are treated. 529 and Coverdell withdrawals are tax-free if used on qualified expenses; all Trump Account withdrawals are taxed. Some states also offer tax deductions or tax credits for 529 plan contributions.

One unique feature of Trump Accounts is a one-time federal contribution of $1,000 for eligible children born 2025 to 2028 when an account is opened on their behalf. Coverdell and 529 do not receive any federal contributions.

Contribution Limits

Coverdell ESAs and Trump Accounts both have federal contribution limits, while 529 plan limits vary by state.

Coverdell ESA has a maximum contribution of $2,000 annually and any donors must make under a certain household income to contribute (currently under $110k for a single filer and $220k for a joint filer). Trump Accounts have a maximum annual contribution of $5,000, and employers can contribute an additional $2,500.

529 contribution limits are state-dependent. Some states, like California and Texas, have no annual contribution limits. Almost all states have lifetime limits, generally around $500k (Wyoming has no lifetime limit).

Another key difference: Coverdell ESAs and Trump Accounts stop accepting contributions once the child turns 18, while 529 plans can be contributed to indefinitely.

Compatibility

Each account type offers rollover options that help families retain any unused funds.

Coverdells can roll into 529s, so the money can be used tax-free for career upskilling. If funds remain unused by age 30, the money is taxed and released to the beneficiary.

529s can roll over to ABLE and Roth IRAs. ABLE accounts are for individuals with disabilities and can be used lifelong to cover various expenses. Up to $35k can also be rolled over to a Roth IRA, jumpstarting retirement savings.

Trump Accounts can roll over to ABLE, just like 529s. Since they are inherently child retirement accounts, any unused funds are treated like those in a Traditional IRA.

Picking the Right Child Savings Account

There are many things to consider when picking a child savings account and only you know your circumstances. Choosing the right savings account depends on your family’s goals, financial situation, and priorities.

Consider questions like:

- Was my child born in 2025 to 2028?

- Is my child under 18 years old?

- Do I want tax-free withdrawals?

- Do I want to be able to use funds on their K-12 education?

- Is flexibility beyond education expenses important?

- Do I want unused funds to support retirement later in life?

- Does my income qualify me to contribute to a Coverdell ESA?

- Will rollover flexibility matter for my family?

Anyone can have a 529 plan, but only children under 18 can have a Coverdell ESA or Trump Account opened for them. If your child is eligible, you can certainly have all three! The main thing to consider is how to build up savings.

How to Build Child Savings

Saving for the future shouldn’t fall entirely on one person. Contributions for future savings can come from a combination of sources: yourself, your community, and even your employer.

1. Set Aside Funds

Build regular savings into your budget to make future goals manageable. Setting up recurring transfers can make saving easier and more consistent.

Better yet, automate contributions straight from payroll. With Paidly’s employer benefit, you can automatically direct a portion of your paycheck toward 529 savings. That keeps the money from hitting your bank account, minimizing the temptation to use the money elsewhere.

2. Crowdfund with Your Community

Community support can also play a meaningful role, especially during birthdays, holidays, graduations, and other milestones. Asking for monetary contributions around these special times lets loved ones contribute to your child’s future.

Paidly allows families to crowdfund 529 savings directly. Our platform sends funds straight to the account so your donors know money will end up where intended. Plus, donors don’t need a login to donate, making it an easy yet meaningful way to show they care.

3. Get Employer Benefits

Your benefits package could also be supporting your efforts. Employers can contribute to Coverdells, 529s, and Trump Accounts. Some 529s even give them tax-advantages.

Ask your HR department about college savings assistance. If they don’t have it yet, suggest Paidly. We let your employer send funds directly to your child’s 529 through recurring or one-time contributions.

All yours in just a few taps

Gain financial awareness and take control of your debt, savings, and donations. Paidly is a convenient, connected way to get ahead with no pay-to-download or hidden fees.

Deciding to Save is the First Step

There’s no one-size-fits-all approach to saving for a child’s future. The right account depends on how you plan to use the funds, your tax priorities, and the level of flexibility you want long term.

Whether you choose a 529 plan, a Coverdell ESA, a Trump Account, or a combination of all three, starting early makes a meaningful difference in reducing future financial stress and expanding opportunities for your family.

Team Paidly

Paidly is the go-to platform for rising above student debt. We specialize in innovative solutions, such as employer student loan assistance benefits, streamlined 529 plan contributions, and crowdfunding tools for individuals and their families. Backed by nearly two decades of experience in financial technology, Paidly is committed to simplifying student loan repayment, reducing loan dependency, and empowering students to take control of their finances no matter where they are in their educational journey.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.

How the Big Beautiful Bill Affects Student Savings

OBBBA expanded 529 plan uses, made ABLE provisions permanent, and introduced Trump Accounts. Here’s what you need to know.