What is a 529 Plan? The Secret Weapon for College Savings

Investing in your child's future education is a wise decision. A 529 plan offers a tax-advantaged way to save for those costs.

Key Takeaways

- A 529 plan is a tax-advantaged investment account to save for education expenses during K-12, college, or student loan repayment.

- There are two types: education savings plans and prepaid tuition plans, with different investment options and tax benefits.

- Contributions are after-tax but grow tax-deferred; withdrawals are tax-free for qualified expenses and flexible if a child doesn't attend college.

- While investment returns fluctuate, 529 plans carry relatively low risk compared to other college savings vehicles.

Saving for a child's education is a major financial commitment. 529 plans provide a flexible and tax-efficient way to save for future college costs. Understanding these plans is crucial due to the rising cost of higher education.

What is a 529 Plan?

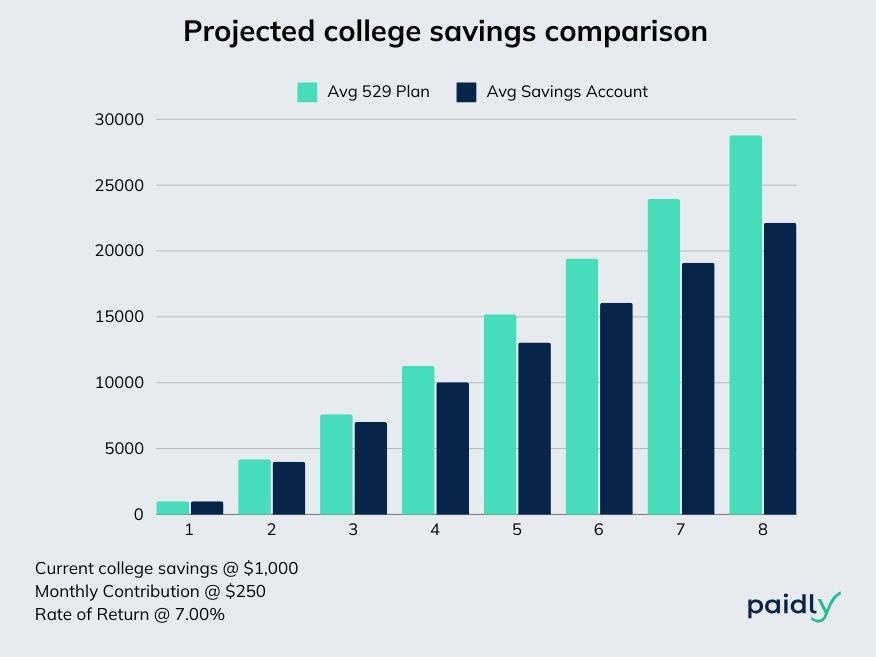

A 529 plan is a state-sponsored, tax-advantaged investment account designed to encourage saving for future education expenses. These plans offer tax-free growth for education-related expenses and can be opened for yourself, your child, or another family member.

Flexible and Useful for Varied Educational Needs:

-

Education Expenses: 529 covers tuition, fees, supplemental education, placement and achievement testing, and essential supplies like textbooks from K-12 through college.

-

Technology: Funds can be used to purchase a computer, install needed software, or make internet payments if being used for study.

-

Assistance: 529 also covers equipment and educational therapies (like occupational, behavioral, physical, and speech-language) for students with special needs.

-

Living Costs: On-campus room and board, off-campus housing, and meal plan expenses are also covered.

-

Additional Paths: 529 plans support dual-enrollment programs, apprenticeship programs, licensure costs, continuing education, and student loan repayments.

Key Benefits

529 plans offer tax-efficient ways to save for education. Contributions grow tax-deferred, and withdrawals for qualified expenses are tax-free. Many states provide additional benefits like tax deductions or credits for contributions.

Tax Advantages: Save More for Education

529 plans come with impressive tax perks, making them an attractive choice for anyone aspiring to save for educational needs. Many states even offer extra benefits like tax deductions or credits for contributions to their 529 plans.

Types of 529 Plans

There are two primary types of 529 plans:

-

Education Savings Plans These allow you to save for qualified education expenses at any eligible institution. Funds grow tax-deferred, and withdrawals are tax-free if used for qualified expenses. They offer more flexibility but carry investment risks.

-

Prepaid Tuition Plans These let you lock in future tuition rates at today’s prices. They are less flexible and are limited to specific institutions but protect against rising tuition costs.

The main difference between the two types lies in their investment approach and the flexibility they offer. Savings plans are more versatile but carry investment risk, while prepaid plans offer tuition cost protection but are limited to specific institutions.

How 529 Plans Work

To open a 529 account, select a plan sponsored by a state or educational institution. Contribute funds regularly or as lump sums, which are then invested in options like mutual funds or ETFs. Contributions grow tax-deferred, and withdrawals for qualified expenses are tax-free.

Choosing the Right 529 Plan

Consider your state’s tax benefits when choosing a 529 plan, though you can opt for any state’s plan. Decide whether an age-based portfolio, which becomes more conservative as college approaches, or a risk-based portfolio, which remains consistent according to your risk tolerance, suits you best. Be mindful of fees and investment options.

Pros and Cons of 529 Plans

Advantages:

-

Tax benefits: Contributions grow tax-deferred; withdrawals for qualified expenses are tax-free.

-

Flexibility: Funds can be used for various education expenses, including K-12 tuition and student loan repayments.

-

Low maintenance: These plans are convenient for long-term savings.

Disadvantages:

-

Limited investment options: Choices may not align with your risk tolerance or goals.

-

Penalties for non-qualified withdrawals: If funds are withdrawn for non-qualified expenses, you'll typically owe income tax plus a 10% penalty on the earnings portion per Bankrate.com.

-

Fees and expenses: Various fees can reduce returns over time.

529 Plan Contribution Limits

In 2024, you can contribute up to $18,000 per student without incurring gift taxes. Lifetime contribution limits range from $235,000 to $550,000, depending on your state.

Investment Options for 529 Plans

529 plans offer three main investment options:

-

Age-Based Portfolios: Automatically become more conservative as the beneficiary approaches college age.

-

Risk-Based Portfolios: Maintain a steady risk level based on your tolerance.

-

Individual Investment Portfolios: Customize your investment mix with mutual funds, ETFs, and money markets.

Most 529 plans give you a mix of options including stocks, bonds, and money markets. Whether these investments are from home or abroad, they work together to help you reach your college savings goals.

Using 529 Plan Funds

529 plan funds can be used to cover a wide range of qualified education expenses, including tuition, fees, books, supplies, and certain room and board costs. According to the U.S. News & World Report, some other eligible expenses include computers, internet access, and certain education loan repayments.

However, it's important to note that non-qualified withdrawals from a 529 plan are subject to income tax and a 10% penalty on the earnings portion of the withdrawal. As Fidelity advises, it's crucial to keep good records and plan ahead to ensure that withdrawals are used for qualified expenses.

If there are any leftover funds after the beneficiary completes their education, SavingForCollege.com suggests several options, such as transferring the funds to another beneficiary, using them for qualified education loan repayments, or even withdrawing the funds (subject to taxes and penalties on the earnings portion).

What happens to the 529 If a Child Doesn't Go to College?

If your child decides not to attend college or use the funds in their 529 plan, you have several options:

-

Change the Beneficiary: Most 529 plans allow you to change the beneficiary to another eligible family member, such as a grandchild, niece, or nephew, once per year without penalty. This way, the funds can still be used for educational expenses.

-

Use for Other Qualified Education Expenses: 529 plan funds can be used for various qualified education expenses beyond just college tuition, such as trade schools, apprenticeship programs, student loan repayments, and even K-12 tuition (subject to annual limits).

-

Non-Qualified Withdrawals: If you choose to withdraw the funds for non-educational purposes, you'll owe income tax on the earnings portion of the withdrawal, plus a 10% penalty on those earnings. However, the principal contribution amount can be withdrawn without penalty.

-

Roll Over to Another 529 Plan: You can roll over the funds from one 529 plan to another for the same beneficiary once every 12 months without triggering taxes or penalties.

Starting in 2024, if there's any money left in a 529 savings plan after college, or if college isn't in the plans at all, that money can now help kick start retirement savings by moving it into a traditional or Roth IRA. This is a big bonus, allowing for smart future planning with any leftover funds. It's a great way to make sure every dollar saved works hard, even beyond college years.

Is It Risky to Have a 529 Plan?

While 529 plans offer significant tax advantages for college savings, they come with certain risks. One risk is market risk, as the investment options within a 529 plan are subject to market fluctuations. The value of your investments can decrease, potentially reducing the amount available for education expenses.

Another risk is the potential for changes in federal or state laws governing 529 plans. These changes could affect tax benefits, contribution limits, or other aspects of the plans. It's essential to stay informed about any legislative updates that may impact your 529 plan.

Additionally, 529 plans typically offer limited investment options, which may not align with your risk tolerance or investment goals. You have less control over the investment choices within the plan compared to other investment vehicles.

Tax Benefits of 529 Plans

One of the primary advantages of 529 plans is their tax-advantaged status. Contributions to a 529 plan are made with after-tax dollars, but the money grows tax-deferred, allowing for potentially higher returns over time. Additionally, qualified withdrawals from a 529 plan are entirely tax-free when used for eligible education expenses, such as tuition, fees, books, and room and board.

Many states also offer state income tax deductions or credits for contributions to their respective 529 plans, providing an additional tax incentive for residents. However, it's important to note that state tax benefits may vary, and some states may not offer any deductions or credits.

Overall, the tax advantages of 529 plans can help families save more for their children's education by reducing the impact of taxes on their investment growth and withdrawals.

Getting Started with a 529 Plan

Opening a 529 plan is relatively straightforward. You can open an account directly with your state's 529 plan provider or through a financial advisor. When opening an account, you'll need to provide some basic information about yourself and the beneficiary (the future student).

Once the account is open, you'll need to select your investment options. Most 529 plans offer a variety of portfolio options, ranging from aggressive stock funds to conservative bond funds or age-based portfolios that automatically adjust as the beneficiary gets closer to college age. It's important to consider your risk tolerance and investment timeline when choosing investments.

You'll also want to set up a contribution schedule that works for your budget. Many plans allow you to set up automatic transfers from your bank account on a schedule that suits you. It's generally advisable to start saving as early as possible to take full advantage of compound growth over time.

Employers Direct Contributions to Employees Children’s 529 College Saving Plans

As you plan for your child's educational future, it's important to consider all available options. While a 529 plan can be a powerful tool for saving for college expenses, it's crucial to remember that student loan debt can be a significant burden for many families. That's where Paidly comes in – a unique solution that allows employers to directly contribute to their employees' children’s 529 college saving plans.

If you are late to start saving for your children's college savings, be sure to read our Late to Save? 529 Strategies for Parents.

Still have questions? We have answers! Talk to an Expert today or send us an email at [email protected].

Team Paidly

Paidly is the go-to platform for rising above student debt. We specialize in innovative solutions, such as employer student loan assistance benefits, streamlined 529 plan contributions, and crowdfunding tools for individuals and their families. Backed by nearly two decades of experience in financial technology, Paidly is committed to simplifying student loan repayment, reducing loan dependency, and empowering students to take control of their finances no matter where they are in their educational journey.

Stay Ahead of the Curve

Get the latest insights on student loan repayment, 529 contributions, and maximizing employer benefits delivered to your inbox.

The information provided is of a general nature and an educational resource. It is not intended to provide advice or address the situation of any particular individual or entity. Any recipient shall be responsible for the use to which it puts this document. Paidly shall have no liability for the information provided. While care has been taken to produce this document, Paidly does not warrant, represent or guarantee the completeness, accuracy, adequacy, or fitness with respect to the information contained in this document. The information provided does not reflect new circumstances, or additional regulatory and legal changes. The issues addressed may have legal, financial, and health implications, and we recommend you speak to your legal, financial, and health advisors before acting on any of the information provided.

You may also like

ABLE Accounts and 529 Plans: A Flexible Savings Strategy

Learn how 529 plans and ABLE accounts work together to make your savings even more supportive.

Maximizing Your Total Rewards Budget

How to offset stagnant wages with tax-advantaged benefits – making a 1% raise feel like 3%.

How the Big Beautiful Bill Affects Student Savings

OBBBA expanded 529 plan uses, made ABLE provisions permanent, and introduced Trump Accounts. Here’s what you need to know.